Blockchain Technology Explained

A SIMPLE GUIDE

Blockchain Technology Explained

+ how it relates to Bitcoin. Written from a completely non-technical perspective.

Defining Blockchain Technology

Blockchain technology is a type of distributed ledger technology (DLT) — It is an accounting system where the ledger (record of transactions) is distributed among a network of computers.

So at its core, blockchain technology is a record-keeping tool.

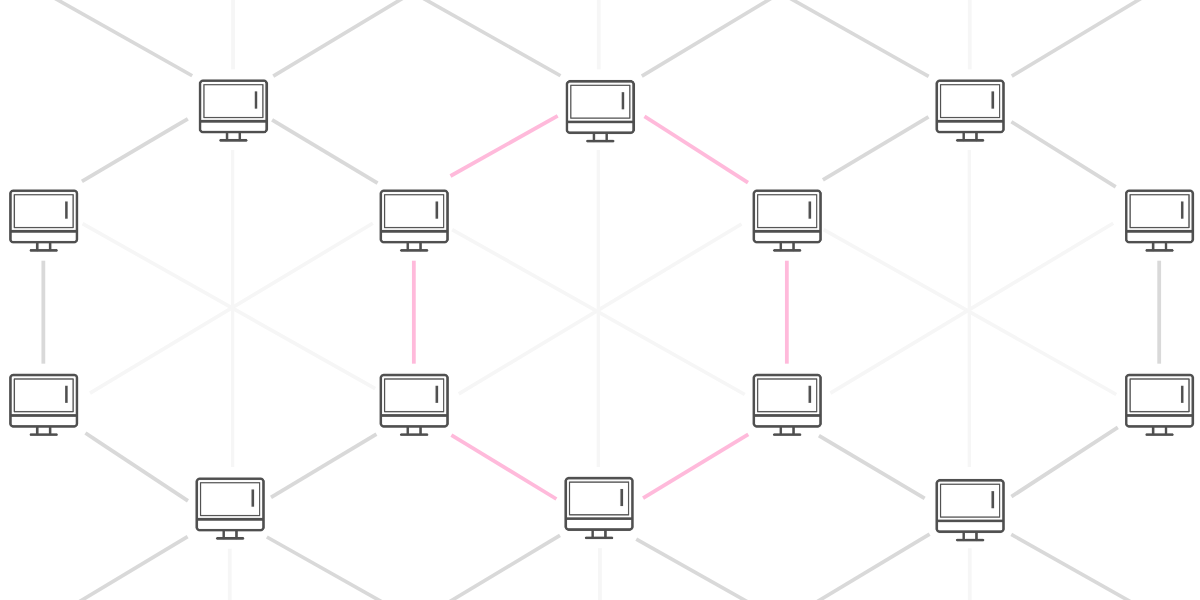

This network of computers all manage the blockchain together without hierarchy (refer to header image). With such a flat architecture, blockchain networks are often referred to as peer-to-peer networks.

First, these computers verify all transactions one by one and add them onto a ‘block’ of information. Then these blocks are added to the blockchain and downloaded onto each computer. In a nutshell, this is how these computers keep the blockchain secure and running.

TL:DR — a blockchain is a digital ledger of transactions that is managed and owned by a peer-to-peer network of computers.

Breaking it down

The term blockchain refers to the fact that it is a ‘chain’ of ‘blocks’. A ‘chain’ because everything is recorded in chronological order. And ‘blocks’ because the transactions are added to the chain in groups rather than individually.

‘Block’

Each block records a number of transactions, similar to a page in a record-keeping book. The amount of transactions on a block varies from blockchain to blockchain. For example, each block on the Bitcoin blockchain holds up to 1 megabyte of information.

‘Chain’

These transactions are recorded in the form of hashes — strings of numbers and letters. The hash of each transaction is generated to include information from the current and past transactions. This creates a chain effect where the order of hashes cannot be changed. As a result, transactions are immutable once they’ve been added.

All transactions need to be verified before they are added onto the blockchain. This is done through a consensus mechanism, which allows all the nodes on the network to agree on things without an authority. This is how blockchains stay autonomous and decentralized.

[

What is consensus algorithm? - Definition from WhatIs.com

A consensus algorithm is a process in computer science used to achieve agreement on a single data value among…

whatis.techtarget.com

](https://whatis.techtarget.com/definition/consensus-algorithm)

For an in-depth, but still easy-to-understand explanation of blockchain technology, this is a great guide:

[

How Blockchain Technology Works. Guide for Beginners

Nearly everyone has heard of Blockchain and that it is cool. But not everybody understands how it works. This article…

cointelegraph.com

](https://cointelegraph.com/bitcoin-for-beginners/how-blockchain-technology-works-guide-for-beginners#hash-function)

What makes blockchain technology unique?

- Decentralized: Because blockchains are managed by a network of nodes rather than a central authority, they are fully decentralized. This prevents any one entity from having any control over the network.

- Transparent: Transactions on a blockchain are constantly being recorded and stored on the blockchain across nodes. This means that all participants can view all transactions on the network in real-time.

- Immutable: Blockchains are designed to enable permanent record keeping so that stored data cannot be altered after being added. This makes it an extremely stable and reliable record-keeping system.

- Secure: It is hard to change or destroy blockchains because of its distributed nature. For example, if someone hacked into one of the computers on the network and altered information there, the network would remain unaffected.

How does Bitcoin fit into all this?

In 2009, Satoshi Nakamoto introduced the world to Bitcoin. His goal was to create a peer-to-peer payment network that would remove the need for a 3rd party to verify these transactions.

Before Bitcoin, the only way people could exchange money digitally was through a bank, exchange or online service. These are all examples of 3rd parties that control our information, money and transaction records.

To solve this problem, Satoshi described the use of blocks connected in a chain that was chronological and permanent. This solved the double-spend problem and allowed people to exchange money knowing their transactions were secure and irreversible. This became what we now know as blockchain technology.

As the first cryptocurrency, Bitcoin spurred the creation of other cryptocurrencies that are all attempting to solve specific problems. For example, Monero was created to provide a completely anonymous network (bitcoin is only pseudonymous). Ether was created to power an open-source platform for decentralized applications. And Dash was created to allow for quicker digital transactions.

Blockchain applications

Since then, blockchain technology has evolved to not only be applicable to financial transactions, but also be useful in other types of peer-to-peer transactions. Anything that involves exchanging information, data or products can be verified and recorded on a blockchain.

The bigger question is whether we need to remove current 3rd parties from these transactions. The truth is, blockchain technology is not a solution for everything, so it’s important to weight the pros and cons of using it.

I explore this issue in more detail here:

[

Blockchain Needs Selfless People

Why we aren’t seeing progress despite the massive potentials , and how we should be thinking about blockchain adoption

medium.com

](https://medium.com/swlh/what-blockchain-needs-is-selflessness-5286501c9d4a)

Explore more like this

Một cá voi chi 6 triệu USD mua NFT

Thị trường NFT sôi động trở lại khi nhiều cá voi đang ra sức chi tiền mua các NFT.

Comments